It boils down to this: Trump/Musk/DOGE are basically stealing the tax money that New Yorkers send to Washington which the federal government is obligated to send back to pay the Social Security, Medicare, Medicaid benefits and other social services that are cumulatively funded by the federal government. And they are stealing that money from the most vulnerable people – the elderly, the disabled, children, veterans, the sick and the poor – in order to further enrich the richest in society.

Out of New York’s $292 billion budget, 40% – $92 billion – is supposed to come back to the states from the federal taxes we pay. Indeed, a “donor state”, New Yorkers pay more into the federal coffers than come back to us, while Red States like Louisiana, Mississippi and Alaska that boast of their low taxes, get way more in federal funding than they pay in income taxes.

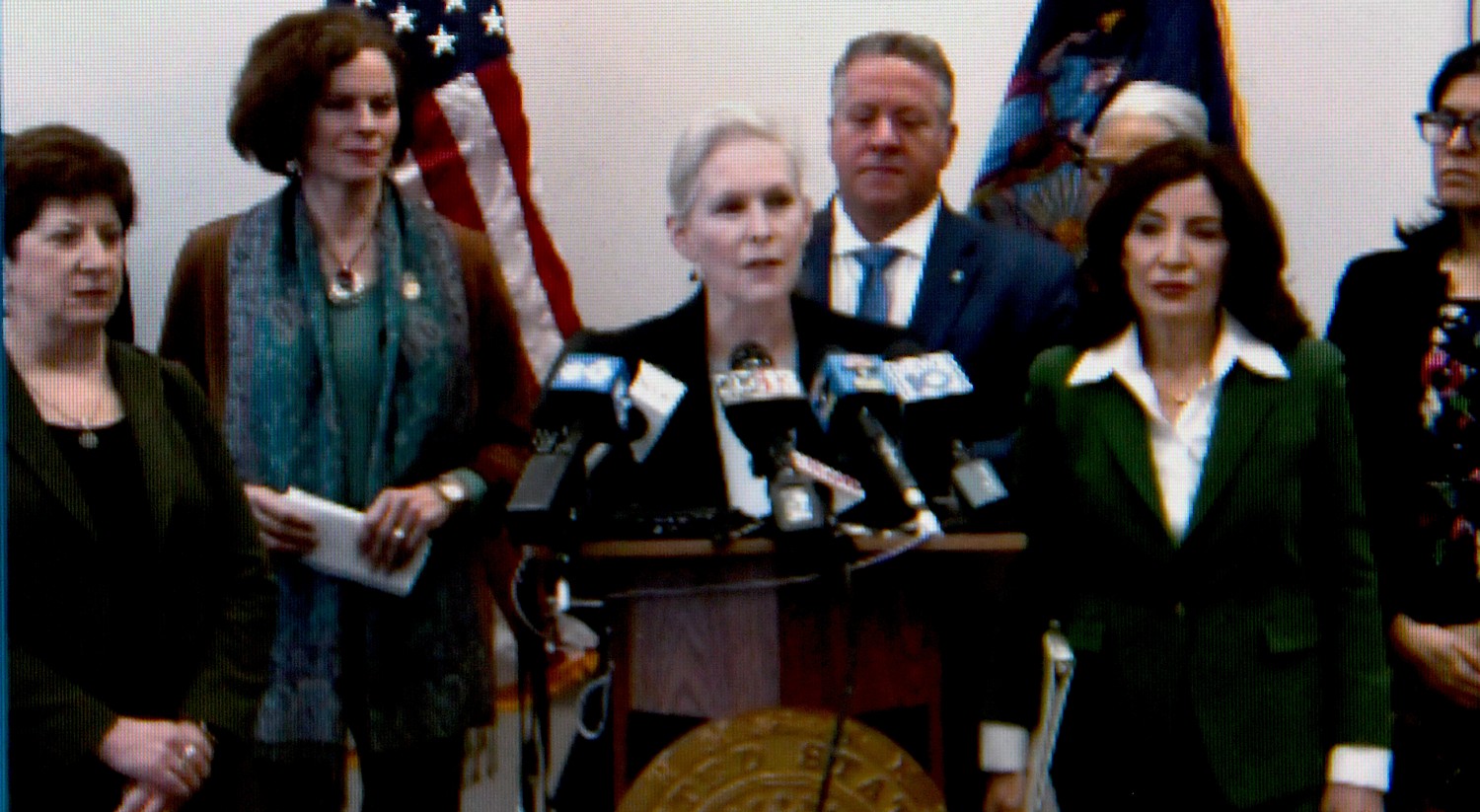

What’s worse is the random, casual, careless way the cuts are being made. “He throws spaghetti to the wall, and what falls down is what’s cut,” Governor Kathy Hochul said at a press conference with US Senator Kirsten Gillibrand to focus attention on the damage being caused to Social Security.

“The Trump administration and DOGE boys are crippling phone support even though appointments can only be made by phone; they plan to cut 7000 staff even though staff numbers are already at a 50 year low; they cut 47 Social Security locations including two in New York State. Meanwhile, 10,000 each day turn 65, all entitled to their earned benefits,” declared U.S. Senator Kirstin Gillibrand.

The cuts in service and the ability to access benefits could be catastrophic, Gillibrand said, “for seniors, people with disabilities who rely on social security to pay for rent, food, heating, medical care – everything they need to survive.” Social security is this nation’s largest anti-poverty program, and arguably its most popular government program.

But it also directly impacts their family and has rippling effect on the economic wellbeing of their community and the state.

“Imagine the impact on New York’s economy if they can’t buy essentials, can’t afford healthcare. It puts greater burden on hospitals, clinics…That doesn’t just affect them, but the community, businesses, services, the entire economy.”

Over 4 million New Yorkers receive Social Security, of which 125,000 are children/ In Albany, alone, 70,000 receive social security. It amounts to $128 million.

Damage has already been done, Gillibrand said. Phone services already in disarray, there is chaos and fear, especially for people unable to travel in person.

“Many of these changes are so severe, more drastic, more radically harmful than ever imagined, I don’t think people fully comprehend. It’s deeply destabilizing. As harm continues to affect every citizen, people will start calling their representative and make them understand their adherence and loyalty to one man is at odds with their constituents, hopefully will then stop,” Senator Gillibrand said.

“We as a society decided government would provide a safety net. If we go back to that time when safety nets don’t exist, more will die in poverty.

“The good news is we have a strong state government strong, but the state budget is affected. We pay so much in federal tax dollars, we expect them to come back to the state. If our federal dollars don’t come back, that means chunks are taken from health care, social security administration, disability. We have to rise up, to convince the seven Republicans to change their mind, to convince Republican senators to stop standing by Trump,” Gillibrand said.

The state was in the final stages of adopting its budget when Trump slashed spending that was already factored in, and there is no way the state can make up for the hole being dug by rescission of federal funds.

“This man [Elon Musk] has enormous power for an unelected official, and he is using it to destroy the very fabric of our safety nets — programs like Social Security,” declared Governor Hochul. “So, he has caused so much chaos and uncertainty. Just walk into this federal building — you can feel it, it’s palpable; the anxiety that the workers here who dedicate their lives to public service, not just here, but all across this country, are under siege. Why? Because they’re out there helping the people.

“That is the whole premise behind becoming a public servant, and those who work for Social Security know that there’s people who rely on them and not everybody knows how to go online and figure it out…..When phone calls aren’t answered, when offices are closed — the offices that have been closed in New York State already — that requires seniors who may not have easy access to get around to go from their community and travel across five to seven different counties. How are they going to get there if they need services in person?

“In New York, our priorities are different,” Governor Hochul said. “We think it’s wrong to say seniors and people with disabilities have to travel a great distance to secure their benefits. We say it’s wrong to describe Social Security as a ‘Ponzi scheme,’ and we say it’s wrong to jeopardize a safety net that has been there to make sure that our citizens never slip into poverty.”

What’s to be done?

Governor Hochul urged constituents to pressure New York State’s seven Republican Members of Congress.

“They are your Republican members of Congress. They’re in the majority, they have the power. If seven members of the delegation from New York State — starting with Elise Stefanik all the way on down — go into the Speaker’s office, demand that there would be changes or you’ll hold up President Trump’s agenda. You have the power, and if you don’t use that power, then you are complicit in this attack on the American people. And so, citizens, residents, people who represent all of our elected officials here: Make sure our voices are heard, make sure our senior’s voices are heard and we have to stop the insanity of this attack on our people.”

Harm to State’s Health Programs

Governor Kathy Hochul also shared a breakdown of the Trump administration’s sweeping federal cuts to New York State’s health programs, and how these cuts to health funding will affect New Yorkers. The amount of funding lost will have a devastating impact statewide on programs that ensure the safety and well-being of people in New York, gutting over $360 million in financial resources toward mental health and addiction services, and health departments across the State.

“Slashing funding for public health, suicide prevention and addiction services is just plain cruel, and it’s going to hurt everyday New Yorkers most,” Governor Hochul said. “Here’s the sad truth: there is no State in the nation that has the resources to backfill these sweeping cuts. It’s up to New York’s elected officials who serve in the House majority to stand up and fight back.”

Federal Cuts by the Numbers:

Department of Health: DOH expects to lose over $300 million in funding for organizations across the State.

This funding supports many activities that are core to public health functioning, including virus surveillance, outbreak response, electronic data exchange, public dashboards, infection prevention activities in hospitals and nursing homes, laboratory reporting, program operations, and support to local health departments. The backbone of the State’s public health infrastructure will be weakened significantly due to reduced virus surveillance and reporting systems that can no longer provide communities and families with real-time information on developing outbreaks, laboratory support and testing, data collection and analysis, public-facing dashboards, data and analytics.

Losing this funding will shutter multiple areas of work that are largely seen as foundational components of the Department’s response to emerging infectious diseases. These cuts will also eliminate the Centers for Disease Control (CDC) and Prevention’s COVID-19 Health Disparities Grant, which funded 135 subcontractors to support community-based work addressing health disparities in New York, such as mental health, maternal and infant health, and food security.

Office of Addiction Services and Supports: OASAS expects to lose $40 million total in funding, which will result in significant cuts to addiction and prevention services, treatment supports and access to resources for individuals struggling with substance use. This work includes, but is not limited to:

Transitional housing to help provide short-term housing and case management for individuals leaving OASAS residential treatment or correctional facilities who cannot otherwise access permanent housing.

Support for programs, access to treatment, recovery, and other basic services that keep people connected to care in their communities.

Expansion of outpatient clinics to offer medication for addiction treatment and to purchase and outfit mobile medication units to bring services where they are needed.

Administering and implementing Screening, Brief Intervention, and Referral to Treatment (SBIRT) which is a comprehensive public health approach to identify those at risk of developing substance use disorders and deliver early intervention and treatment services to individuals who exhibit habits of risky use of alcohol and other substances.

Office of Mental Health: OMH expects to lose $27 million total in funding for programs and services for individuals experiencing mental health and/or substance use needs. These programs were intended to allow individuals in need of care to remain in their homes, connected to their natural support systems during treatment. The loss of this funding will result in an increased reliance on emergency services and hospital-based care with fewer community resources and supports for our most vulnerable New Yorkers, including:

Crisis Stabilization and Crisis Residence Programs to provide urgent treatment to individuals experiencing an acute mental health and/or substance use crisis, and a safe place for the stabilization of psychiatric symptoms and support for children and adults.

Adult Assertive Community Treatment Teams (ACT) serving individuals with serious mental illness who are in danger of losing their housing/becoming homeless, are homeless, and/or have histories of involvement with the criminal justice system, and Children and Youth Assertive Community Treatment Teams (ACT) for youth who are returning home from inpatient settings or residential services, at risk of entering such settings, or have not adequately engaged or responded to treatment in more traditional community-based services.

Grants to expand and improve upon the mobile crisis services statewide, including 9-8-8 crisis call centers. These call centers have relied on this funding to ensure they have capacity to connect callers experiencing emotional distress to the compassionate care of trained counselors.

New York State Department of Health Commissioner Dr. James McDonald said, “It is disappointing these grants were terminated so impulsively without any advance notice and without consideration for the people we serve. We were poorly prepared as a nation for the last pandemic. I see the same pattern occurring now, where decisions are made without consideration for the public’s health and well-being. These grants were preparing us to be healthier for the next pandemic. These investments allowed New York to develop strategies that prevent chronic disease, improve nutrition and find problems before they started.”

“These sweeping federal cuts to health and human services threaten critical addiction funding streams that support prevention, harm reduction, treatment, and recovery services, putting lives at risk and straining the providers working tirelessly on the frontlines of this public health crisis,” Office of Addiction Services and Supports Commissioner Dr. Chinazo Cunningham said. “OASAS remains committed to protecting and expanding access to life-saving services, and will work to mitigate the damage caused by these harmful cuts.”

Office of Mental Health Commissioner Dr. Ann Sullivan said, “For many years, the federal government has been a trusted and valued partner in efforts to provide critical mental health services and supports to New Yorkers, many living in traditionally marginalized communities and under difficult socioeconomic conditions. These drastic cuts will likely slow, and in some instances, halt the fantastic progress our federally funded programs have made and continue to make across our state. We have come too far to reverse course on mental health, which is why our federal legislators owe it to New York to challenge these cuts however possible.”

This fact sheet analyzing the House Republicans’ proposed 2025 budget that would target Medicare, Social Security, the Affordable Care Act (Obamacare), repeal caps on drugs and cut taxes for the wealthy, is provided by the White House:

In his State of the Union Less than two weeks ago, President Biden laid out his vision for an economy that gives the middle class a fair shot. He also warned that congressional Republicans “will cut Social Security and give more tax cuts to the wealthy,” that they continue to oppose the Affordable Care Act, and that they are siding with Big Pharma over hardworking families.

On Wednesday, Republican Study Committee – which represents 100% of House Republican leadership and nearly 80% of their members – just proposed yet another budget that would cut Medicare, Social Security, and the Affordable Care Act , as well as increase prescription drug, energy, and housing costs – all while forcing tax giveaways for the very rich onto the country. Their plan would even raise the Social Security retirement age.

Like President Biden promised in the Capitol, “If anyone here tries to cut Social Security or Medicare or raise the retirement age I will stop them.”

He’s keeping that promise by standing against this new House Republican budget. He knows the last thing we should do is raid Medicare and Social Security while giving more giant tax cuts to the wealthy and big corporations.

What’s more, House Republicans’ plan would raise energy costs and send our new manufacturing jobs back overseas by gutting other crucial elements of the Inflation Reduction Act, raise housing costs, and allow big companies to rip off consumers with junk fees.

President Biden has a different vision for how we move into the future: make the wealthy, big corporations, and special interests pay their fair share while protecting and strengthening Medicare and Social Security. Extending the Affordable Care Act tax credits he delivered to lower health care costs and cover more Americans than any time in history. Making the economy work for the middle class by investing in America and the industries of the future, while lowering key costs that working families face. And expanding Medicare’s ability to negotiate lower drug costs.

80% of House Republicans released a Budget that:

Cuts Medicare and Social Security while putting health care at risk for millions

Calls for over $1.5 trillion in cuts to Social Security, including an increase in the retirement age to 69 and cutting disability benefits.

Raises Medicare costs for seniors by taking away Medicare’s authority to negotiate prescription drug costs, repealing $35 insulin, and the $2,000 out-of-pocket cap in the Inflation Reduction Act

Transitions Medicare to a premium support system that CBO has found would raise premiums for many seniors.

Cuts Medicaid, the Affordable Care Act, and the Children’s Health Insurance Program by $4.5 trillion over ten years, taking coverage away from millions of people, eroding care for seniors, children, and people with disabilities, and taking us back to the days where people could be denied care for pre-existing conditions and charged more for health insurance simply for being a woman.

Rigs the economy for the wealthy and large corporations against middle class families

Passes $5.5 trillion in tax cuts skewed to the wealthy and large corporations, including permanently extending tax cuts in the Trump tax law, repealing the minimum tax on billion-dollar corporations the President signed into law, eliminating the estate tax for the wealthiest Americans, providing a massive tax cut for billionaire investors, and making it easier for the wealthy and large corporations to get away with cheating on their taxes.

Kills jobs and investment in communities throughout the country – including Red States – by eliminating the clean energy tax credits in the Inflation Reduction Act.

Makes it easier for companies and banks to rip consumers off with unfair and hidden junk fees by eliminating the Consumer Financial Protection Bureau.

Raises housing costs by cutting funding for rental assistance, cutting funding for programs that help build housing, and raising mortgage costs for first-time homebuyers.

In response to the Republican budget plan, President Biden issued a statement : “My dad had an expression, ‘Don’t tell me what you value. Show me your budget, and I’ll tell you what you value.’ The Republican Study Committee budget shows what Republicans value. This extreme budget will cut Medicare, Social Security, and the Affordable Care Act. It endorses a national abortion ban. The Republican budget will raise housing costs and prescription drugs costs for families. And it will shower giveaways on the wealthy and biggest corporations. Let me be clear: I will stop them.

“My budget represents a different future. One where the days of trickle-down economics are over and the wealthy and biggest corporations no longer get all the breaks. A future where we restore the right to choose and protect other freedoms, not take them away. A future where the middle class finally has a fair shot, and we protect Social Security so the working people who built this country can retire with dignity. I see a future for all Americans and I will never stop fighting for that future.”

This fact sheet on the impact on health care coverage, benefits and protections under the Congressional Republicans’ plans was provided by the White House:

President Biden’s top priority is to lower costs for the American people. He was proud to sign the Inflation Reduction Act into law, taking on Big Pharma to allow Medicare to negotiate prescription drug costs for the first time, capping seniors’ drug costs at the pharmacy and the cost of insulin, and lowering health insurance premiums for people who get coverage through the Affordable Care Act. President Biden and Congressional Democrats are committed to protecting and strengthening Social Security and Medicare.

Congressional Republicans have a very different vision. They have promised to strip Medicare of the right to negotiate drug prices and remove the $2,000 cap on out-of-pocket pharmacy expenses. Florida’s Republican Senator and Chair of the National Republican Senatorial Committee Rick Scott has championed a plan to put Medicare, Medicaid, and Social Security on the chopping block every five years. Further, Congressional Republicans have repeatedly pledged to hold the American economy hostage by refusing to raise the debt limit unless they can cut Social Security and Medicare benefits that tens of millions of Americans have already paid into.

Here’s what Congressional Republicans’ plan would mean:

Part I: Putting Bedrock Programs like Social Security and Medicare on the Chopping Block and Threatening the Global Economy Unless Those Programs Are Cut

All Medicare, Medicaid, and Social Security beneficiaries would see their benefits threatened under Sen. Rick Scott’s plan to put those programs on the chopping block every five years. Sen. Ron Johnson’s vision of putting them up for a vote every year would make that even worse.

Congressional Republican leaders have also repeatedly said they will use the debt limit as leverage to cut these bedrock programs. Congressional Republicans have supported Medicare and Social Security cuts including:

Transforming Medicare benefits into a voucher where seniors would get a fixed amount of money to purchase a private health plan (Better Way Plan) or offering beneficiaries the option to transition to a premium support system (Republican Study Committee FY 2023 Budget) – which could lead to hundreds or thousands of dollars in additional out of pocket costs for seniors throughout the country.

Part II: Repealing the Prescription Drug and Health Care Provisions in the Inflation Reduction Act

President Biden has worked for decades to let Medicare negotiate drug prices, and that is finally happening thanks to the Inflation Reduction Act. This will save billions of dollars for both Medicare beneficiaries, who will see reduced premiums and out-of-pocket costs, and the federal government. Kaiser Family Foundation estimates suggest that some 5 to 7 million beneficiaries each year use the types of high-cost drugs that could be subject to negotiation and will directly face higher cost sharing if these provisions are repealed.

The Inflation Reduction Act also requires prescription drug companies to pay rebates if they increase drug prices faster than inflation. According to an analysis by the Department of Health and Human Services, the cost of 1,200 prescription drugs rose faster than inflation in the last year alone – some prescription drugs increasing by $1000 in just one year. If Congressional Republicans repeal the Inflation Reduction Act, drug companies will be able to continue raising prices without paying a rebate, rather than putting that money back into Americans’ pockets.

Before the Inflation Reduction Act, Medicare beneficiaries with conditions like cancer, multiple sclerosis, and lung disease could face thousands of dollars in out-of-pocket prescription drug costs per year. Thanks to President Biden and Congressional Democrats’ Inflation Reduction Act, those costs will be capped at $2,000 per year, saving over 1 million beneficiaries an average of over $1,300 per year. If Congressional Republicans get their way and repeal the law, over 1.4 million Medicare beneficiaries will pay more each year – thousands of dollars more in some cases – for drugs at the pharmacy.

Drug manufacturers have raised insulin prices so rapidly over the last few decades that some Medicare beneficiaries struggle to afford this life-saving drug that costs less than $10 a vial to manufacture. Today, Medicare beneficiaries are enrolling in plans that must cap the out-of-pocket cost of insulin at no more than $35 per month per prescription, a protection they will lose if the law is repealed.

The Inflation Reduction Act saves 13 million Americans an average of about $800 per year on their health care premiums, by continuing the improvements to Affordable Care Act (ACA) premium tax credits enacted in the American Rescue Plan. By making health care more affordable, these improvements have expanded coverage to millions of people, helping bring the uninsured rate to an all-time low. Starting today, during Open Enrollment season, Americans can choose health insurance plans that lock in the Inflation Reduction Act’s cost savings for 2023. But Congressional Republicans would repeal this assistance, drive premiums higher, and jeopardize the progress the Biden Administration has made in driving the uninsured rate to a historic low. Older Americans would see especially large premium spikes; in most states, annual premiums for a 60-year old making $60,000 would more than double to over $10,000.

On Saturday, August 8, Trump signed four Executive Orders intended to substitute for Congressional Republicans compromising with Democrats on a relief package against the health and economic ravages of the coronavirus pandemic. In a vitriolic speech, delivered to a mini-rally assembled from among his Bedminister golf course members, he attacked the Democrats’ plan, threatened a stock market crash should Joe Biden become president, and promised to end the payroll tax (which funds Social Security) should he be elected.

Indeed, Trump delivered this campaign promise: to reduce income taxes and capital gains taxes (in order to goose the stock market), in effect robbing the US Treasury which is already over $25 trillion in debt with trillions added because of the 2017 GOP tax cuts and the trillions spent on COVID relief, much of it going to the wealthiest and best connected. Instead of providing aid to states and localities which have been devastated by depleted revenues and run-up in costs to address COVID-19, he put more of the burden on states to come up with his faux employment benefits (it requires 25% to be paid by states). Instead of funding election protection and the post office, he accused Democrats of stealing the election.

“The massive taxpayer bailout of badly run blue states we talked about — that’s one of the things they’re looking to do. Measures designed to increase voter fraud,” he told his adoring audience.

“You know what it’s about? Fraud. That’s what they want: fraud. They want to try and steal this election because, frankly, it’s the only way they can win the election.

“The bill also requires all states to do universal mail-in balloting — which nobody is — nobody is prepared for — regardless of whether or not they have the infrastructure. They want to steal an election. That’s all this is all about: They want to steal the election.”

Trump couldn’t resist attacking proposals for a Green New Deal: “And they want to do the Green New Deal, which will decimate our country and decimate — it’s ridiculous, too. It’s childish. I actually say the Green New Deal is childish. It’s for children. It’s not for adults.”

And when asked what happens if the states can’t pony up the 25% to continue the $400 (not $600) unemployment benefits (the 75% that the federal government would spend would be coming from the states’ share of the CARES Act funding), he said, “Well, if they don’t, they don’t…So I don’t think their people will be too happy.”

As for the reduction in unemployment benefits, Trump said, “this gives them a great incentive to go back to work.”

Questioned about the constitutionality of going around Congress, which has the sole “power of the purse,” Trump said, “This will go very [fast]– if — if we get sued. Maybe we won’t get sued. If we get sued, it’s somebody that doesn’t want people to get money. Okay? And that’s not going to be a very popular thing. “

Pressed whether a President should go around Congress “ and decide how money is collected and spent?” Trump retorted, “You ever hear the word ‘obstruction’? “yes,” the reporter replied. “You were investigated for that.”

Trump then replied, “They’ve obstructed. Congress has obstructed. The Democrats have obstructed people from getting desperately needed money.”

“But this is in the Constitution, Mr. President,” the reporter insisted.Asked why he keeps taking credit for Veterans Choice, which was passed in 2014 by the Obama Administration, Trump abruptly ended the press conference.

In reaction to Trump’s executive orders, Vice President Joe Biden, presumptive Democratic nominee for President, issued this statement: –Karen Rubin/news-photos-features.com

Unable to deliver for the American people in a time of crisis, Donald Trump offered a series of half-baked measures today. He is putting Social Security at grave risk at a time when seniors are suffering the overwhelming impact of a pandemic he has failed to get under control. And make no mistake: Donald Trump said today that if he is re-elected, he will defund Social Security.

For months, Trump has golfed rather than negotiated, and sown division rather than pull people together to get a package passed. Now, instead of staying in Washington and working with Republicans and Democrats to reach a bipartisan deal, President Trump is at his golf club in New Jersey signing a series of dubious executive orders.

This is no art of the deal. This is not presidential leadership. These orders are not real solutions. They are just another cynical ploy designed to deflect responsibility. Some measures do far more harm than good.

One order is Donald Trump’s first shot in a new, reckless war on Social Security. Trump announced a payroll tax plan with no protections or guarantees — like the ones the Obama-Biden administration enforced a decade ago — that the Social Security Trust Fund will be made whole. And, Trump specifically stated today that if re-elected, he plans to undermine the entire financial footing of Social Security. He is laying out his roadmap to cutting Social Security. Our seniors and millions of Americans with disabilities are under enough stress without Trump putting their hard-earned Social Security benefits in doubt.

Another order brings cuts, chaos, and confusion to our system of unemployment insurance. Trump is unilaterally reducing the amount laid-off workers could receive. And he purports to provide these benefits until the end of the year, but only identifies enough funding to make it a handful of weeks. Even with that limited funding, Trump is basically playing a cruel game of robbing Peter to pay Paul: He is taking billions of dollars of federal natural disaster funding away so it won’t be available to states like Florida. And, he is forcing states to choose between imposing benefit cuts for unemployed workers or slashing funds for public schools, health workers, and first responders.

A third order, on evictions, is woefully inadequate to deal with the emerging housing crisis. He is leaving our nation’s renters with ever-mounting debt and leaving our small family landlords badly squeezed. Without a comprehensive plan to help our American families make rent, they will leave this crisis months behind on their payments while many landlords teeter on the verge of bankruptcy.

And a fourth order is a band-aid approach to student debt that leaves out 7 million borrowers who obtained their federal loans from private lenders or their college rather than the Department. The economic strain on these Americans is deep and unrelenting.

There is a solution to all of this pain and suffering. A real leader would go back to Washington, call together the leaders of the House and Senate, and negotiate a deal that delivers real relief to Americans who are struggling in this pandemic. We need a president who understands their struggle and believes in their courage to overcome.

Whenever Republicans

talk about the need to reform “entitlements,” they always refer to the “sacrifice”

demanded of the people most dependent upon Social Security benefits and most

vulnerable (with the least political power) in society. They never ask the most

obscenely rich, most comfortable, most powerful to make any sacrifice – after all,

they are the “job creators” and we don’t want to interfere with the number of

yachts and vacation homes they can purchase.

Senator Elizabeth

Warren, vying for the 2020 Democratic nomination for president, has just

released her plan to expand Social Security – not cut it.

“Millions of Americans

are depending on Social Security to provide a decent retirement. My plan raises

Social Security benefits across-the-board by $2,400 a year and extends the full

solvency of the program for nearly another two decades, all by asking the top

2% to contribute their fair share to the program,” Warren states. “It’s time

Washington stopped trying to slash Social Security benefits for people who’ve

earned them. It’s time to expand Social Security.”

This is from the

Warren campaign:

Charlestown, MA – Today, Elizabeth Warren

released her plan to provide the biggest and most progressive increase in

Social Security benefits in nearly 50 years. Her plan will mean an immediate

Social Security benefit increase of $200 a month — $2,400 a year — for every current

and future Social Security beneficiary in America. That will immediately help

nearly 64 million current Social Security beneficiaries, including 10 million

Americans with disabilities and their families.

The plan also updates outdated rules to further increase

benefits for lower-income families, women, people with disabilities,

public-sector workers, and people of color. The plan finances these benefit

increases and extends the solvency of Social Security by nearly two decades by

asking the top 2% of earners to contribute their fair share to the

program.

According to an independent analysis,

Elizabeth’s plan will immediately lift an estimated 4.9 million seniors out of

poverty — cutting the senior poverty rate by 68%. It will also produce a “much

more progressive Social Security system” by delivering much larger benefit

increases to lower and middle-income seniors on a percentage basis,

increase economic growth in the long term, and reduce the deficit by

more than $1 trillion over the next 10 years.

I’ve dedicated most of my career to studying what’s happening to working families in America. One thing is clear: it’s getting harder to save enough for a decent retirement.

A generation of stagnant wages and rising costs for basics

like housing, health care, education, and child care have squeezed family

budgets. Millions of families have had to sacrifice saving

for retirement just to make ends meet. At the same time, fewer people have

access to the kind of pensions that used to help fund a comfortable retirement.

As a result, Social Security has become the main source of

retirement income for most seniors. Abouthalf of married

seniors and 70% of unmarried seniors rely on Social Security for at least half

of their income. More than 20% of married seniors and 45% of unmarried

seniors rely on Social

Security for 90% or more of their income. And the numbers are

even more stark for seniors of color: as of 2014, 26% of Asian and Pacific

Islander beneficiaries, 33% of Black beneficiaries, and 40% of Latinx

beneficiaries relied on Social Security benefits as their only source of retirement income.

Yet typical Social Security benefits today are quite small.

Social Security is an earned benefit — you contribute a portion of your wages

to the program over your working career and then you and your family get

benefits out of the program when you retire or leave the workforce because of a

disability — so decades of stagnant wages have led to smaller benefits in retirement

too. In 2019, the average Social Security beneficiary received $1,354 a month, or

$16,248 a year. For someone who worked their entire adult life at an average

wage and retired this year at the age of 66, Social Security will replace just 41% of what

they used to make. That’s well short of the 70% many financial

advisers recommend for a decent retirement — one that allows you to keep living

in your home, go to a doctor when you’re sick, and get the prescription drugs

you need.

And here’s the even scarier part: unless we act now, future

retirees are going to be in even worse shape than

the current ones.

Despite the data staring us in the face, Congress hasn’t

increased Social Security benefits in nearly fifty years. When

Washington politicians discuss the program, it’s mostly to debate about whether

to cut benefits by a lot or a little bit. After signing a $1.5 trillion tax

giveaway that primarily helped the rich and big corporations, Donald Trump

twice proposedcutting billions

from Social Security.

We need to get our priorities straight. We should be

increasing Social Security benefits and asking the richest Americans to

contribute their fair share to the program. For years, I’ve helped lead the fight in

Congress to expand Social Security. Andtoday I’m

announcing a plan to provide the biggest and most progressive increase in

Social Security benefits in nearly half a century. My plan:

Increases Social Security benefits immediately by $200 a

month — $2,400 a year — for every current and future Social Security

beneficiary in America.

Updates outdated rules to further increase benefits for

lower-income families, women, people with disabilities, public-sector workers,

and people of color.

Finances these changes and extends the solvency of Social

Security by nearly two decades by asking the top 2% of families to contribute

their fair share to the program.

An independent analysis of my plan

from Mark Zandi, chief economist of Moody’s Analytics, finds that my plan will

accomplish all of this and:

Immediately lift an estimated 4.9 million seniors out of

poverty, cutting the senior poverty rate by 68%.

Produce a “much more progressive Social Security system”

by raising contribution requirements only on very high earners and increasing

average benefits by nearly 25% for those in the bottom half of the income

distribution, as compared to less than 5% for people in the top 10% of the

distribution.

Increase economic growth in the long term and reduces the

deficit by more than $1 trillion over the next ten years.

Every single current Social Security beneficiary — about 64

million Americans — will immediately receive at least $200 more per month under

my plan. That’s at least $2,400 more per year to put toward home repairs, or

visits to see the grandkids, or paying down the debt you still might owe. And

every future beneficiary of Social Security will see at least a $200-a-month

increase too, whether you’re 60 years old and nearing retirement or 20 years

old and just entering the workforce. If you want to see how my plan will affect

you, check out my new calculator here.

Our Current Retirement Crunch — And How It Will Get Worse

If We Don’t Act

Seniors today are already facing a difficult retirement.

Without action, future generations are likely to be even worse off.

While we’ve reduced the

percentage of seniors living in poverty over the past few decades, the numbers

remain unacceptably high. Based on the U.S. Census Bureau’s Supplemental

Poverty Measure, 14% of seniors —

more than 7 million people — live in poverty. Another 28% of seniors have

incomes under double the poverty line. A record-high 20% of seniors are still in the workforce in

their retirement years. Even with that additional source of income, in 2016,

the median annual income for

men over 65 was just $31,618 — and just $18,380 for women over 65.

It’s hard to get by on that, especially as costs continue to

rise. Most seniors participate in Medicare Part B, and standard premiums for

that program now eat up close to 10% of the average monthly Social Security benefit.

The average senior has just 66% of Social

Security benefits remaining after paying all out-of-pocket healthcare expenses

— and if we don’t adopt Medicare For All, out-of-pocket medical spending by

seniors is projected to rise sharply over

time. The number of elderly households still paying off debt has grown by

almost 20% since 1992,

and hundreds of thousands of

seniors have had their monthly benefits garnished to pay down student loan

debt.

Meanwhile, the prospect of paying for long-term care looms

over most retirees. 26% of seniors

wouldn’t be able to fund two years of paid home care even if they liquidated

all of their assets. And for people that have faced lifelong discrimination,

like LGBTQ seniors who until recently were denied access to spousal pension

privileges and spousal benefits, the risk of living in or near poverty in

retirement is even higher.

This squeeze forces a lot of seniors to skimp in dangerous

and unhealthy ways. A recent survey found that

millions of seniors cut pills, delay necessary home and car repairs, and skip

meals to save money.

While the picture for current retirees is grim, it’s

projected to get even worse for Americans on the cusp of retirement. Among

Americans aged 50 to 64, the average amount saved in 401(k) accounts is less

than $15,000. On average,

Latinx and Black workers are less likely to have

401(k) accounts, and those who do have them have smaller balances and are more

likely to have to make withdrawals before retirement. The gradual disappearance

of pensions has been particularly harmful to

workers of color who are near retirement. And 13% of all people

over 60 have no pension or savings at all.

Meanwhile, this near-retirement group are also suffering

under the weight of mounting debt levels and other costs. 68% of households headed

by someone over 55 are in debt. Nearly one-quarter of

people ages 55 to 64 are also providing elder care. According to one study, 62%

of older Latinx workers, 53% of older Black workers, and 50% of older Asian

workers work physically demanding jobs,

leading to higher likelihood of disability, early exit from the job market, and

reduced retirement benefits.

Gen-Xers and Millennials are in even greater trouble. For

both generations, wages have been virtually stagnant for

their entire working lives. 90% of Gen-Xers are

in debt, and they’re projected to be able to replace only 50% of their income

in retirement on average. Many Gen-Xers are trapped between

their own student loans and mortgages, the costs

of raising and educating their

children, and the costs of caring for their elderly relatives. Two-thirds of

working millennials have no retirement savings, and the numbers are even worse

for Black and Latinx working millennials. Debt, wage stagnation, and decreasing

pension availability mean that, compared to previous generations at the same

age, millennials are significantly behind in

retirement planning.

There’s also the looming prospect of serious Social Security

cuts in 2035. Social Security has an accumulated reserve of almost $3 trillion

now, but because of inadequate contributions to the program by the rich, we are

projected to draw down that reserve by 2035, prompting automatic 20% across-the-board

benefit cuts if nothing is done.

My plan addresses both the solvency of Social Security and

the need for greater benefits head on — with bold solutions that match the

scale of the problems we face.

Creating Financial Security By Raising Social Security

Benefits

The core of my plan is simple. If you get Social

Security benefits now, your monthly benefit will be at least $200 more — or at

least $2,400 more per year. If you aren’t getting Social Security benefits now

but will someday, your monthly benefit check with be at least $200 bigger than

it otherwise would have been.

My $200-a-month increase covers every Social Security

beneficiary — including the 10 million Americans

with disabilities and their families who have paid into the program and now

receive benefits from it. Adults with disabilities are twice as likely to

live in poverty as those without a disability. While 9% of people

without disabilities nearing retirement live in poverty, 26% of people that

age with disabilities live in poverty. Monthly Social Security benefits make up

at least 90% of income for

nearly half of Social Security Disability Insurance beneficiaries.

This benefit increase will also provide a big boost to other

groups. It will help the 621,000 disabled

veterans who are Social Security beneficiaries. It will benefit the 1 million seniors

who exclusively receive Social Security Insurance — which helps Americans with

little or no income and assets — and the 2.7 million Americans

who receive both SSI and Social Security benefits.

On top of this across-the-board benefit increase, I’ll

ensure that current and future Social Security beneficiaries get annual

cost-of-living adjustments that keep pace with the actual costs they face. The

government currently increases Social Security benefits annually to keep pace with the

price of goods typical working families buy. But older Americans and people

with disabilities tend to purchase more of certain goods — like health care —

than working-age Americans, and the costs of those goods are increasing more

rapidly. That’s why my plan will switch to calculating annual cost-of-living increases

based on an index called CPI-E that better

reflects the costs Social Security beneficiaries bear. Based on current

projections, that will increase benefits

even more over time.

Combined, my immediate $200-a-month benefit increase for

every Social Security beneficiary and the switch to CPI-E will produce

significantly higher benefits now and decades into the future. My Social

Security calculator will let you see how much your benefits could change under

my plan.

Targeted Social Security Improvements to Deliver Fairer

Benefits

Broadly speaking, Social Security benefits track with your

income during your working years. That means pay disparities and wrongheaded

notions that value salaried work over time spent raising children or caring for

elderly relatives carry forward once you retire. That needs to change. My plan

increases Social Security benefits even further by making targeted changes to

the program to deliver fairer benefits and better service to women and

caregivers, low-income workers, public sector workers, students and

job-seekers, and people with disabilities.

Women and Caregivers

In part because of work and pay discrimination and

time out of the workforce to provide care for

children and elderly relatives, women receive an average monthly Social

Security benefit that’s only 78% of the average

monthly benefit for men. That’s one reason women over the age of 65 are 80% more likely to

live in poverty than men. My plan includes several changes that primarily

affect women and help reduce these disparities.

Valuing the work of caregivers. My plan creates

a new credit for caregiving for people who qualify for Social Security

benefits. This credit raises Social Security benefits for people who

take time out of the workforce to care for a family member — and recognizes

caregiving for the valuable work it is.

The government calculates Social Security benefits based on

average lifetime earnings, with years spent out of the workforce counted as a

zero for the purpose of the average. When people spend time out of the

workforce to provide care for a relative, their average lifetime earnings are

smaller and so are their Social Security benefits.

That particularly harms lower-income women, people of color,

and recent immigrants. There are more than 43 million informal

family caregivers in the country, and 60% of them are

women. A 2011 study found that women over fifty forgo an average of $274,000 in

lifetime wages and Social Security benefits when they leave the workforce to

take care of an aging parent. Caregivers who also work are more likely to be

low-income and incur out-of-pocket costs for providing care. Because access to

paid or partially paid family leave is particularly limited for workers

of color — and first-generation immigrant workers are less likely to have

jobs with flexible schedules or paid sick days — these workers are more likely

to have to take unpaid leave to provide care and thus suffer reductions in

their Social Security benefits.

My plan will give credit toward the Social Security average

lifetime earnings calculation to people who provide 80 hours a month of unpaid

care to a child under the age of 6, a dependent with a disability (including a

veteran family member), or an elderly relative. For every month of caregiving

that meets these requirements, the caregiver will be credited for Social

Security purposes with a month of income equal to the monthly average of that

year’s median annual wage. People can receive an unlimited amount of caregiving

credits and can claim these credits retroactively if they have done this kind

of caregiving work in the last five years. By giving caregivers credits equal

to the median wage that year, this credit will provide a particular boost in

benefits to lower-income workers.

Improving benefits for widowed individuals from

dual-earner households and widowed individuals with disabilities. Because

women on average outlive men by 2.5 years, they

typically spend more of their retirement in widowhood, a particularly vulnerable period financially.

My plan provides two targeted increases in benefits for widows.

In households with similar overall incomes, Social Security

provides more favorable survivor benefits to the surviving spouses in

single-earner households than in dual-earner households. After the death of a

spouse, a surviving spouse from a dual-earner household can lose as much

as 50% of her

household’s retirement income. My plan will reduce this disparity by ensuring

that widow(er)s automatically receive the highest of: (1) 75% of combined

household benefits, capped at the benefit level a household with two workers

with average career earnings would receive; (2) 100% of their deceased spouse’s

benefits; or (3) 100% of their own worker benefit.

My plan will also improve benefits for widowed individuals

with disabilities. Currently, a widow with disabilities must wait until she is

50 to start claiming Social Security survivor benefits if her spouse dies — and

even at 50, she can only claim benefits at a highly reduced rate. Since most

widows with disabilities can’t wait until the official retirement age of 66 to

claim their full survivor benefits, their average monthly benefit is only $748 a month, or

less than $9,000 a year. My plan will repeal the age requirement so

widow(er)s with disabilities can receive their full survivor benefits at any

age without a reduction.

Lower-Income Workers

My plan ensures that workers who work for a lifetime at low

wages do not retire into poverty.

In 1972, Congress enacted a Special Minimum Benefit for

Social Security. The benefit was supposed to help people who had earned

consistently low wages over many years of work. But it’s become harder to

qualify for the benefit, and the benefit amount has shrunk in value so it now helps

hardly anyone. Today, only 0.6% of all

Social Security beneficiaries receive the Special Minimum Benefit, and projections show

that no new beneficiaries will receive it this year.

No one who spends 30 years working and contributing to

Social Security should retire in poverty. That’s why my plan restructures the

Special Minimum Benefit so that more people are eligible for it and the

benefits are a lot higher. Under my plan, any person who has done 30

years of Social Security-covered work will receive an annual benefit of at

least 125% of the federal poverty line when they reach retirement age. That

means a baseline of $1,301 a

month in 2019 — plus the $200-a-month across-the-board increase in my plan, for

a total of $1,501 a month. That’s more than $600-a-month

more than what that worker would receive under current law.

Public Sector Workers

My plan also ensures that public sector workers like

teachers and police officers get the full Social Security benefits they’ve

earned.

If you work in the private sector and earn a pension, you’re

entitled to your full pension and your full Social Security benefits in

retirement. But if you work in state or local government and earn a pension,

two provisions called the Windfall Elimination Provision and Government Pension

Offset can reduce your Social Security benefits. WEP slashes Social Security

benefits for nearly 1.9 million former

public-sector workers and their families, while GPO reduces — and in most cases,

eliminates — spousal and survivor Social Security benefits for 700,000 people, 83% of whom are

women.

My plan repeals these two provisions, immediately

increasing benefits for more than two million former public-sector workers and

their families, and ensuring that every current state and local government

employee will get the full Social Security benefits they’ve earned.

Students and Job Seekers

My plan also updates the Social Security program so that it

encourages people to complete college and participate in job training programs

or registered apprenticeships.

Restoring and extending benefits for full-time students

whose parent has a disability or has died. In the Reagan administration,

Congress cut back a provision that allowed children receiving Social Security

dependent benefits to continue to receive them until age 22 if they were

full-time students. Before the provision was repealed, these beneficiaries came

from families with average incomes 29% lower than their college peers, were

more likely to have a parent with low educational attainment, and were more likely to be

Black. Access to these benefits boosted college

attendance and performance by letting low-income students reduce the number of

hours they had to work while attending school. When Congress repealed this

benefit, college attendance by previously eligible beneficiaries dropped by

more than one-third. My plan

restores this provision — and it extends eligibility through the age of 24

because only 41% of all students

complete college in four years, and Black, Native American, and Latinx students

have even lower four-year

completion rates. A longer eligibility period will improve the chances the

people who receive this benefit complete college before the benefit ends.

Encouraging registered apprenticeships and job training.

Currently, workers who participate in registered apprenticeships or job

training may receive lower Social Security benefits because they are taking

time out of the workforce or agreeing to accept lower-paying positions to gain

skills. We’re about to enter a period of immense transformation in the economy,

and we should encourage workers to take time to participate in a registered

apprenticeship or job training program so they are prepared for in-demand jobs.

That’s why I proposed a $20 billion investment in high-quality apprenticeships

in my Economic Patriotism and Rural America plans.

My plan today complements that investment by letting workers in job training

and apprenticeship programs elect to exclude up to three years in those

programs from their lifetime earnings calculation for Social Security benefits,

thereby producing a higher average lifetime earnings total — and higher

benefits.

Improving the Administration of Social Security Benefits

My plan improves Social Security in another important way:

it makes it easier for people to actually get the benefits they’ve earned.

Congress is starving the Social Security Administration of

money, creating hardship for people who rely on the program for benefits.

Congress has slashed SSA’s operating budget by 9% since 2010, even as

the number of beneficiaries is growing. Meanwhile, more Baby Boomers are

approaching retirement age — a critical period when workers are most likely to

claim Social Security Disability benefits. SSA has a staff shortage, rising telephone

and office wait times, and outdated technology.

Sixty-four Social Security field offices have closed since 2011 and 500 mobile

offices have closed since

2010. Field office closures are correlated with a 16% drop in

disability insurance beneficiaries in the surrounding area because those people

— who have paid into the system and earned their benefits — no longer have assistance

to file their applications.

Disability insurance applicants can wait as long as 22 months for an

eligibility hearing. Thousands of people have

died while waiting for administrative law judges to determine if they’re eligible

to receive their benefits. To make matters worse, Donald Trump issued an

Executive Order that will politicize the

process of selecting the judges who adjudicate these cases. And his

administration keeps proposing more cuts to the

SSA budget.

My plan restores adequate funding to the Social Security

Administration so that it can carry out its core mission. That will allow us to

hire more staff, keep offices open, reduce call times, update the technology

system, and give applicants and beneficiaries the services they need. And I

will revoke Trump’s Executive Order on administrative law judges.

Strengthening Social Security By Extending Solvency For

Nearly Two More Decades

Currently, the rich contribute a far smaller portion of

their income to Social Security than everyone else. That’s wrong, and it’s

threatening the solvency of the program. My plan fully funds its new benefit

increases and extends the full solvency of Social Security for nearly 20 more

years by asking the richest top 2% of families to start contributing more.

Social Security is funded by mandatory insurance

contributions authorized by the Federal Insurance Contributions Act, or “FICA”.

The FICA contribution is 12.4% of wages, with employers and employees splitting

those contributions equally at 6.2% each. (Self-employed workers contribute the

full 12.4%.) If you’re a wage employee, you contribute 6.2% of your very first

dollar of wages to Social Security, and 6.2% of every dollar after that — up to

an annual cap. This year’s cap is $132,900, and each year, that cap increases

based on the growth in national average wages.

Congress designed the cap to go up each year based on

average wages to ensure that a fairly steady percentage of total wages in

America were subject to the FICA contribution requirement. But growing wage

disparities over the past few decades has thrown the system out of whack.

While wages for lower-income and middle-income workers have

been fairly stagnant —

limiting the growth of the national average wage figure we use to set the

annual cap — income at the very top has been skyrocketing. That means

more income for the biggest earners has been above the cap and therefore exempt

from the FICA contribution requirement. In 1983, 90% of total wage

earnings were below the cap. Now it’s just 83%. The top 1% of

earners have an estimated effective

FICA contribution rate of about 2%, compared to more than 10% for the middle

50% of earners. That amounts to billions of dollars every year that should have

gone to Social Security but instead remained in the pockets of the very richest

Americans, while the Social Security system slowly starved.

And the very rich have escaped contributing to the system in

yet another way: more and more of their income is in the form of unearned

investment income, not wages, and they don’t have to contribute any of their

investment income to Social Security. Although most Americans earn most of

their income from wages, capital income makes up more than half of

total income for the top 1% and more than two-thirds for

the top 0.1%. All that income escapes the Social Security program.

My plan brings our Social Security system back into balance

by asking the top 2% of earners to start contributing a fair share of their

wages to the system and by asking the top 2% of families to contribute a

portion of their net investment income into the system as well:

First, my plan imposes a 14.8% Social Security contribution requirement on individual wages above $250,000 — affecting less than the top 2% of earners — split equally between employees and employers at 7.4% each. While most American workers contribute to Social Security with every dollar they earn, CEOs and other very high earners contribute to Social Security on only a fraction of their pay. My plan changes that and requires very high earners to contribute a fair share of their income. My plan also closes the so-called “Gingrich-Edwards” loophole to ensure that self-employed workers can’t easily reclassify income to avoid making Social Security contributions.

Second, my plan establishes a new 14.8% Social Security contribution requirement on net investment income that applies only to the top 2% — individuals making more than $250,000 in annual income or families making more than $400,000 in annual income. My plan creates a new contribution requirement — modeled on the Net Investment Income Tax (NIIT) from the Affordable Care Act — that asks people and families above these high income thresholds to contribute 14.8% of the lesser of net investment income or total income above these thresholds. My plan also closes loopholes in the NIIT that allow wealthy owners of partnerships and other businesses to avoid it. This contribution requirement will ensure that the very wealthy are paying into Social Security even when they report the bulk of their income as capital returns rather than wages.

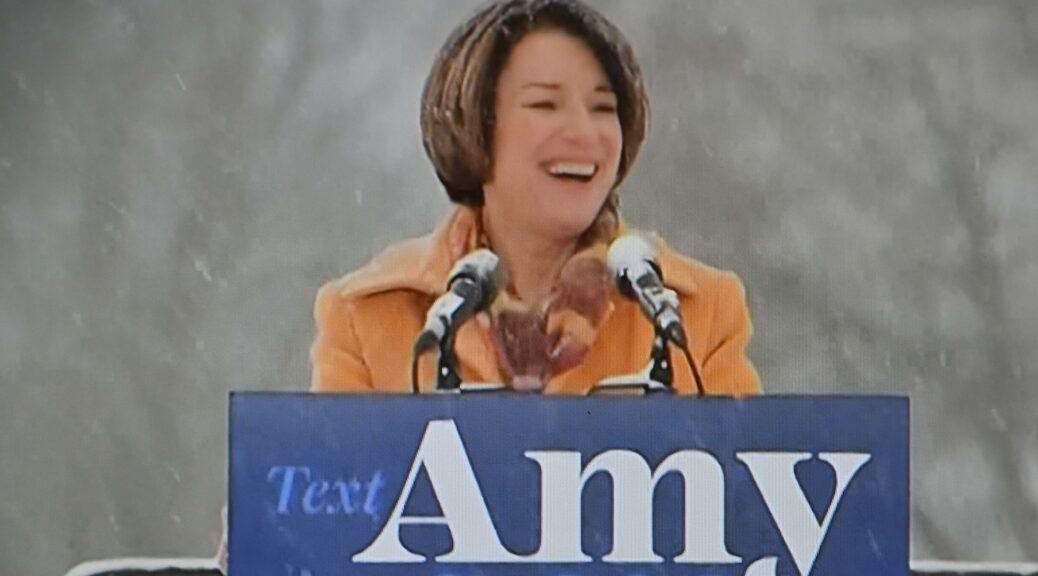

The vigorous contest of Democrats seeking the 2020 presidential nomination has produced excellent policy proposals to address major issues. Senator Amy Klobuchar’s plan for Seniors tackles Alzheimer’s, enhances health care and retirement security and reduces prescription drug costs. This is a summary from the Klobuchar campaign:

MINNEAPOLIS, MN – Senator Amy Klobuchar released her policy priorities for seniors. Building on her leadership in the Senate when it comes

to lowering the cost of prescription drugs and addressing the challenges our

seniors face, Senator Klobuchar is proposing a bold plan to tackle Alzheimer’s

disease and other forms of dementia, enhance health care and retirement

security, reduce skyrocketing prescription drug costs and combat senior fraud

and abuse. As President, Senator Klobuchar will continue to stand up for our

seniors and the 10,000 Americans who turn 65 each day.

“Everywhere I go, I meet seniors who tell me about their struggles to afford

everyday costs like prescription drugs or health care,” said Senator

Amy Klobuchar. “I meet family members who face challenges

caring for loved ones with Alzheimer’s and urgent action is needed to take on

these problems. I believe we owe it to our seniors to make sure they have the

care and support they need as they get older, and as President I will

prioritize tackling Alzheimer’s, strengthening health care and retirement

security, and reducing prescription drug costs.”

Support

caregivers for those living with Alzheimer’s and other chronic conditions.

Senator Klobuchar has been a leader when it comes to supporting people affected

by Alzheimer’s and their families. As President, she will support expanding

resources for health care providers to expand training and support services for

families and caregivers of people living with Alzheimer’s disease or other

forms of dementia as well as other chronic conditions, improving caregiver

well-being and health, as well as allowing patients to stay in their homes

longer.

Make

it easier for people with Alzheimer’s and their families to get the medical

care they need. Medicare is an essential resource for people

affected by Alzheimer’s, but many patients and their families are unaware of

the resources and coverage available when it comes to Alzheimer’s. Senator

Klobuchar will take action to expand Medicare covered services for Alzheimer’s

and she will expand efforts to make patients and their families aware of the

care-planning and services that are covered. She will also support an ongoing

investment in public health infrastructure for Alzheimer’s that reduces risk,

improves early detection and diagnosis, and focuses on tribal, rural, minority,

and other underserved populations.

Strengthen

the National Institutes of Health and invest in research for chronic conditions.

While the current administration has proposed draconian cuts to lifesaving

research, Senator Klobuchar will bolster research at the National Institutes of

Health and increase investments in research into cancer, including breast

cancer, which the Senator has long supported, and other chronic conditions. And

Senator Klobuchar will also invest in research into health disparities.

Significant and persistent disparities exist in health outcomes for minority

populations in the United States. When it comes to healthy aging, research has

shown divides based on race, wealth, and education. Senator Klobuchar will

invest in research across the federal government into the causes of these

disparities and how they can be reduced.

Invest

in Alzheimer’s research.

Senator Klobuchar will commit to preventing, treating and facilitating a cure

for Alzheimer’s disease, with the goal of putting us on a path toward

developing a cure and treatment by 2025. To support researchers, she will make

sure that funding is reliable and consistent. Since African Americans and the

Latino community will represent nearly 40 percent of the 8.4 million American

families affected by Alzheimer’s disease by 2030, Senator Klobuchar will

increase federal research into disparities in the incidents and outcomes of

Alzheimer’s and other forms of dementia.

Improve mental health care for seniors. Senator Klobuchar is committed to making mental health a priority, including for our seniors. As part of her recently released mental health plan, she will expand access to mental health treatment for seniors and expand depression treatment and suicide prevention efforts that focus on seniors.

Implement and extend Kevin and Avonte’s law and expand dementia training. Senator Klobuchar introduced bipartisan legislation signed into law last year that helps families locate missing people with forms of dementia, such as Alzheimer’s, or developmental disabilities, such as autism. As President, Senator Klobuchar will make sure the program is fully implemented and she will also establish federal partnerships with state and local governments to provide dementia training for public sector workers who interact with seniors.

Ensure a Secure Retirement

Protect Social Security and make sure it is fair. Social Security has served as a stable and secure retirement guarantee for generations of Americans. Senator Klobuchar believes that this program must remain solvent for generations to come and she will fight against risky schemes to privatize it. As President, Senator Klobuchar will work to lift the Social Security payroll cap. Currently the payroll tax only applies to wages up to $133,000. Senator Klobuchar supports subjecting income above $250,000 to the payroll tax and extending the solvency of Social Security. And Senator Klobuchar will make sure people are treated fairly by the current Social Security system. As President, she will work to strengthen and improve Social Security benefits for widows and people who took significant time out of the paid workforce to care for their children, aging parents, or sick family members.

Expand retirement savings. Senator Klobuchar believes all Americans deserve a secure retirement. As she has previously announced, Senator Klobuchar will work to create innovative, portable personal savings accounts called Up Accounts that can be used for retirement and emergencies by establishing a minimum employer contribution to a savings plan. [ This proposal is modeled after the Saving for the Future Act, which was introduced by Senators Coons and Klobuchar.] Under her plan, employers will set aside at least 50 cents per hour worked, helping a worker build more than $600,000 in wealth over the course of a career. And Senator Klobuchar will work to reduce disparities when it comes to retirement savings. According to a recent study, the median wealth for white families was more than $134,000, but for African American families it was just $11,000.

Defend pensions. Senator Klobuchar has been a leader in the Senate when it comes to keeping our pension promises. As President, she will support legislation to ensure retirees can keep the pensions they have earned and, in her first 100 days, she will recommend that Treasury heighten the scrutiny of any applications to reduce retiree benefits under the Kline-Miller Multiemployer Pension Reform Act of 2014.

Improve Health Care for Seniors and Lower Prescription Drug Costs

Unleash the power of 43 million seniors in Medicare Part D to negotiate better drug prices. Seniors should have access to their medicines at the lowest possible prices. As President, Senator Klobuchar will push to allow the government to directly negotiate lower drug prices for Medicare Part D, building on legislation she has led in the Senate.

Take immediate and aggressive action to lower prescription drug prices, including allowing personal importation from countries like Canada and crack down on “Pay-for-Delay” agreements. Senator Klobuchar has been a leading advocate for reducing the price of prescription drugs for seniors, including by helping close the Medicare Part D donut hole and introducing legislation to increase competition and require Medicare to negotiate lower drug prices. As President, during her first 100 days she will allow for the personal importation of prescription drugs from safe countries like Canada and crack down on “Pay-for-Delay” agreements that increase the cost of prescription drugs.

Strengthen Medicare and provide incentives for getting the best quality health care at the best price. Senator Klobuchar opposes cuts and risky schemes to privatize Medicare and will take action to strengthen Medicare and find solutions so it remains solvent. She will improve Medicare for current beneficiaries by reforming payment policies through measures like site neutral payments and providing incentives for getting the best quality health care at the best price, including bundled payments and telehealth.

Expand coverage for dental, vision and hearing under Medicare. Dental, vision, and hearing care should be covered as part of Medicare. Senator Klobuchar will support new Medicare coverage for these services that makes them affordable for all seniors.

Expand telehealth and rural health services and maintain rural hospitals. In the Senate, Senator Klobuchar has championed policies that ensure seniors who want to stay in their homes and communities can do so. As President, she will promote remote monitoring technology and telehealth services in Medicare and other programs that improve the quality of life and expand access to quality home care and emergency hospital services in rural areas. As President, she would work to create a new Rural Emergency Hospital classification under Medicare to help rural hospitals stay open and provide expanded support to our critical access hospitals.

Invest in Long-Term Care

Create a refundable tax credit to offset long-term care costs. Senator Klobuchar will work with Congress to establish a new refundable tax credit to help offset the costs of long-term care. The credit will be available for qualifying long-term care costs including both nursing facility care and home- and community-based services, and additional expenses like assistive technologies, respite care, and necessary home modifications. The credit will be targeted towards those who are most in need of support. Senator Klobuchar will also stand up to efforts to cap Medicaid spending, which would put services like mental health care, transportation costs, and long-term care at risk for millions of Americans.

Reduce the costs of long-term care insurance and increase access. Senator Klobuchar believes seniors and their adult children must have the resources they need to prepare for long-term care, including education about the types of services available. To reduce the costs of long-term care, Senator Klobuchar will propose a new targeted tax credit equal to 20 percent of the premium costs of qualified long-term care insurance. Senator Klobuchar will also establish incentives and make it easier for employers to offer their employees long-term care insurance on an opt-out basis. In addition, she will explore updating federal policies to combine long-term care policies with life insurance.

Provide financial relief to caregivers and ensure paid family leave for all Americans, including those who care for elderly or disabled relatives. Senator Klobuchar is proposing a tax credit of up to $6,000 a year to provide financial relief to those caring for an aging relative or a relative with a disability to help offset expenses, including the cost of medical care, counseling and training, lodging away from home, adult day care, assistive technologies, and necessary home modifications. As President, Senator Klobuchar will also support legislation to provide paid family leave to all Americans so no one has to sacrifice a paycheck to care for someone they love, including an elderly parent.

Support a world class long-term care workforce, increase long-term care options, and tackle disparities in long-term care. Senator Klobuchar believes we must invest in and address shortages in our long-term care workforce. She is committed to increasing wages, improving job conditions and promoting other recruitment and retention policies, especially in rural communities facing workforce challenges. She will also support training for long-term care workers and new loan forgiveness programs for in-demand occupations that includes our long-term care workers. In addition, she will expand long-term care facilities and beds as well as home care and telehealth services. Research also suggests that there are significant racial and ethnic disparities in the quality of long-term care as well as disparities in coverage for long-term care. Senator Klobuchar is committed to tackling disparities in care through expanding access to long-term care with a focus on reducing inequities as well as addressing the costs of long-term care services for people in the greatest need of assistance.

Reduce Costs and Prevent Fraud

Fight senior fraud and elder abuse. As a prosecutor, Senator Klobuchar created a senior protection unit at the Hennepin County Attorney’s Office. And she has always believed that we need strong safeguards to prevent and address fraud, abuse and exploitation of our seniors, and has led and passed multiple bills in the Senate that would strengthen these safeguards. Within her first 100 days as President, she will establish a new senior fraud prevention office to educate consumers, expedite the handling of complaints, and coordinate prevention efforts across the federal government. Senator Klobuchar will stregthen enforcement of age discrimination laws, and she will also take action to tackle elder abuse, strengthen oversight and accountability for court-appointed guardians, support training for employees at long-term care facilities, and increase tracking of incidents and investigations to help prevent and better respond to elder abuse.

Improve access to affordable housing, transit, and nutrition for seniors and expand workforce opportunities. In the first 100 days of her Administration, Senator Klobuchar will reverse the Trump Administration’s proposed changes to federal housing subsidies that could triple rent for some households and would be particularly harmful for seniors. In addition, she will update regulations for reverse mortgages to make sure seniors have access to safe products that make it easier to stay in their homes, as well as expand support for affordable senior housing. Senator Klobuchar is also committed to expanding transportation programs and services for older adults, particularly in rural and underserved populations. She also supports expanding resources for Meals on Wheels, helping the food bank system serve seniors in need, and launching a national effort to increase enrollment among seniors in the Supplemental Nutrition Assistance Program. Senator Klobuchar will also work to expand workforce and training opportunities for older Americans who are looking to remain in and return to the workforce.

Help seniors afford their energy costs: Senator Klobuchar strongly opposes efforts by the Trump Administration to eliminate funding for programs like the Low Income Home Energy Assistance Program (LIHEAP), which helps seniors afford heating and cooling. As President, Senator Klobuchar’s budget will preserve and expand resources for LIHEAP and the Weatherization Assistance Program, which helps households in need reduce energy spending, and she will support new efforts to help seniors with their energy costs.

To pay for these policies, Senator Klobuchar will close the trust fund loopholes that allow the wealthy to avoid paying taxes on inherited wealth.

The

vigorous contest of Democrats seeking the 2020 presidential nomination has

produced excellent policy proposals to address major issues. This is from the

Biden 2020 campaign:

THE

BIDEN PLAN FOR OLDER AMERICANS

The moral obligation of our time is rebuilding

the middle class. The middle class isn’t a number, it’s a value set. And, a key

component of that value set is having a steady, secure income as you age so

your kids won’t have to take care of you in retirement. This means not only

protecting and strengthening Social Security, but also helping more

middle-class families grow their savings.